5 min read • published in partnership with Lloyds

Unlocking the next phase of UK manufacturing growth

MACH 2026 saw Lloyds return as headline sponsor, marking over 16 years of continuous support for the event and reaffirming its long-standing commitment to UK manufacturing.

Dave Atkinson, UK Head of Manufacturing, SME & Mid-Corporates at Lloyds, reflects on what the exhibition revealed about a sector defined by capability, ambition and an economic contribution that is often undervalued.

There is nothing quite like stepping into a live manufacturing environment. The hum of machinery, the smell of coolant in the air, seeing swarf spiralling off a cutting tool. For me, it takes me back to being a young lad visiting my dad at work in a sand-casting foundry in the heart of the Black Country.

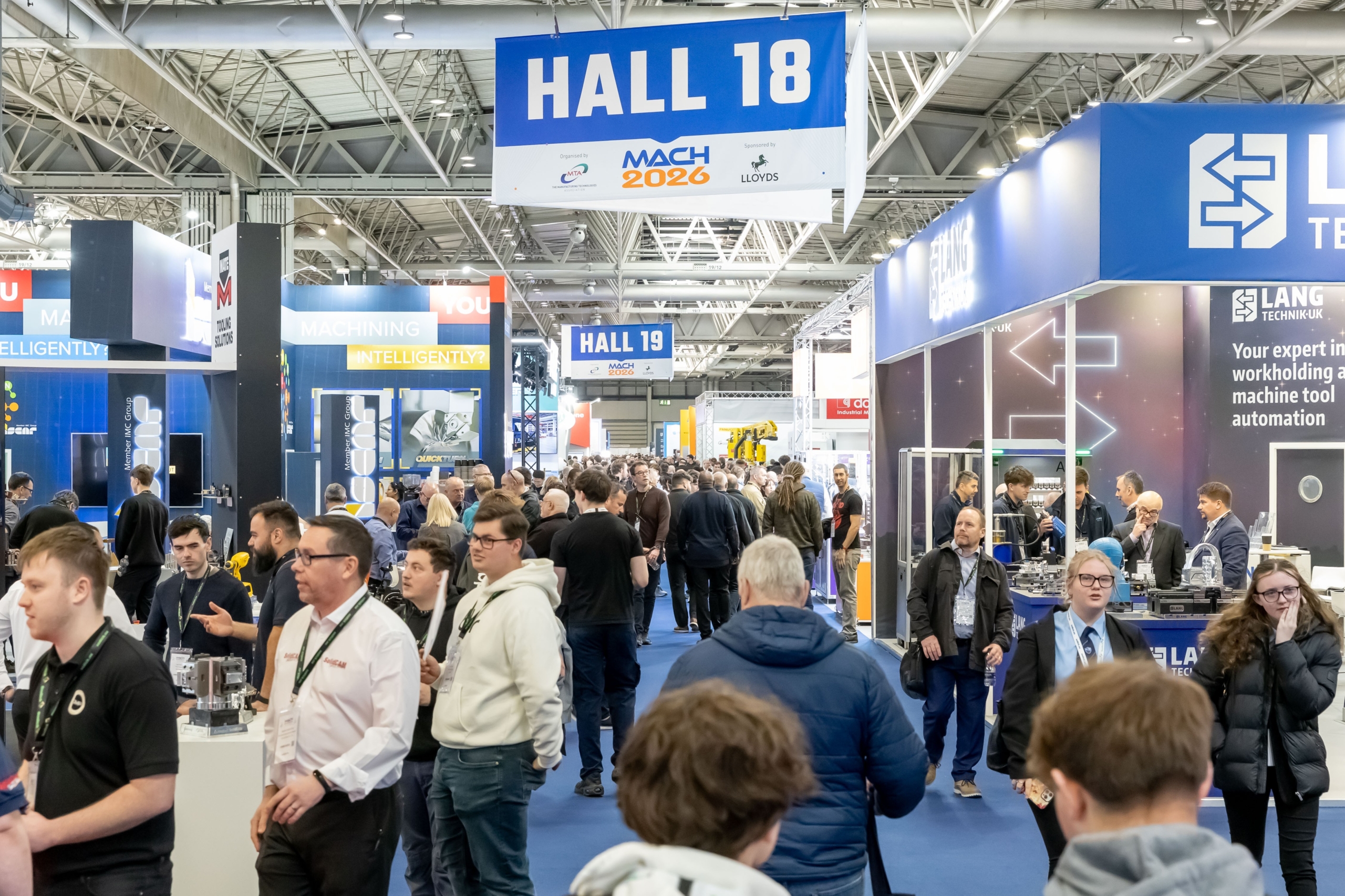

And there is nowhere in the UK that captures that feeling on the same scale as MACH, owned and organised by the Manufacturing Technologies Association (MTA). Held at the NEC Birmingham, this year’s exhibition brought together more than 500 exhibitors showcasing cutting-edge machinery, automation systems, digital technologies and live demonstrations to over 26,000 attendees.

The atmosphere throughout the week was electric, filled with energy, ambition and optimism. There was also a palpable sense of intent. Businesses were actively seeking ways to improve output, reduce price pressures and strengthen operational resilience.

A few days later, a colleague asked whether what I’d seen and heard had restored my confidence in UK manufacturing. I replied that it hadn’t, because I never lost it in the first place.

This is a sector that continues to punch well above its weight. Are there challenges? Of course there are. Energy and operating costs, recruitment pressures, tariff uncertainty, supply chain disruption and cybersecurity risks continue to weigh heavily on industry. But resilience, determination and ingenuity remain defining characteristics of UK manufacturing.

The true scale of manufacturing’s contribution

Too often, manufacturing is described as a shrinking part of the economy, reduced to around 9% of UK GDP compared to almost 25% in the 1970s. But that interpretation grossly understates its true economic impact.

As conventionally measured, manufacturing generates approximately £220bn in GDP and directly employs around 2.6 million people. Yet manufacturers don’t operate in isolation. They rely on extensive networks of suppliers, contractors and service providers spanning logistics and distribution, IT support, maintenance, security, catering, construction, waste management, professional services and beyond.

That network effort creates substantial indirect activity that ripples across the wider economy. There is also the induced impact generated when employees across those supply chains spend their wages in local communities and businesses.

Independent research carried out by Oxford Economics and the MTA, supported by Lloyds, shows that when these effects – direct, indirect and induced impacts – are combined, manufacturing’s total contribution rises to around 23% of GDP and supports more than seven million jobs.

UK manufacturing already accounts for 48% of business R&D and 17% of business investment. Imagine how much further the sector could go if it consistently received the recognition and support befitting its true economic weight.

Skills remain the defining challenge

Despite rapid advances in automation and digitalisation, manufacturing remains fundamentally dependent on people. Technology enhances capability but it’s skilled individuals who convert capability into innovation, problem-solving and continuous improvement.

The sector currently faces around 50,000 live vacancies, a figure largely unchanged year-on-year. One challenge is that manufacturers are no longer only competing with each other for talent. The digitalisation of industry means manufacturing is now competing directly with the tech sector for workers skilled in data science, AI and software architecture.

We often talk about skills in the context of a pipeline, but what’s needed is multiple, overlapping pipelines that tap into previously underutilised or overlooked talent pools, such as the Armed Forces community.

Manufacturing and the Armed Forces share many of the same disciplines: adaptability, technical competence, teamwork, problem-solving under pressure. For service leavers, veterans and reservists looking for purposeful, technically-demanding and rewarding careers, manufacturing is a natural fit. For employers, it offers access to a disciplined, experienced and highly capable talent base.

An exhibitor at MACH 2026 was Service charity Mission Community, which is working with the MTA to support ex-Armed Forces personnel and the wider Service community into manufacturing careers through its Mission Manufacturing programme. The initiative builds on the success of ‘Mission Automotive’ and ‘Misson Renewables’, which have helped hundreds of individuals transition into new roles in these sectors.

The rapidly expanding defence sector also creates significant opportunity for manufacturing beyond talent alone, however.

Higher defence spending creates huge opportunity

One of the clearest industrial investment signals in decades is the government’s commitment to increase defence and national security spending to 5% of GDP by 2035. Defence exports reached a 40-year high of £20bn in 2025, and the sector already works with around 12,000 UK SMEs – with government ambitions to expand participation further, targeting £7.5bn annually by 2028.

What businesses frequently misunderstand is that defence procurement is not limited to advanced military hardware. For example, plans to upgrade 40,000 military homes over the next decade opens substantial demand for building material manufacturers, heating and ventilation specialists and modular housing suppliers. Elsewhere, opportunities will continue to grow for communication systems, digital infrastructure, logistics, textiles, maintenance services and advanced manufacturing capabilities.

For many manufacturers, however, the constraint is not capability but access – and, more broadly, how effectively capacity, skills and investment are aligned to convert demand signals into growth.

Navigating complex procurement processes and accreditation requirements or simply understanding where to start remains a real challenge, particularly for SMEs. Which is why Make UK and Lloyds have developed practical guidance to help businesses better understand where opportunities exist and how to translate capability into opportunity more effectively.

The three-legged stool of productivity

That brings me to one of the biggest themes I took away from MACH 2026 – productivity. We all understand why productivity matters. It drives wealth, raises living standards, strengthens competitiveness and underpins economic growth. If the UK wants a stronger, more resilient economy, improving productivity is a must.

I vehemently believe that productivity rests on three pillars: technology, skills and finance. Think of it as a three-legged stool. If one leg weakens or lags behind, the stool loses balance and inevitably topples.

If businesses have access to finance to invest in the latest machinery and a skilled workforce capable of operating and maintaining it effectively, productivity rises. Capability becomes output. Investment becomes return. Innovation becomes growth.

What MACH does uniquely is put these three elements side by side – investment decisions, technology adoption and skills development interacting within the same industrial ecosystem. Over the five days, across the exhibition floor, businesses could be seen exploring next-generation machinery, discussing funding and investment decisions, and engaging directly with training providers and skills organisations. It is one of the few places where productivity stops being abstract and becomes tangible.

For me, MACH 2026 reinforced that Britain already possesses enormous industrial capability. The focus now needs to be on ensuring these three pillars continue to develop in alignment to unlock the next phase of manufacturing growth.

See how Lloyds is supporting UK manufacturers to innovate, grow and lead here.