2 minute read - 1st November 2022

Subcontract manufacturing sector holds steady in Q3

In the face of rising energy prices, coupled with political and economic uncertainty, the latest Contract Manufacturing Index (CMI) reveals that the UK subcontract manufacturing market held steady in the third quarter of the year. The CMI for Q3 2022 was 102, compared to 101 in Q2 2022, an increase of 1%.

Overall, the market was marginally up on the average level of activity during 2021, but compared to the equivalent quarter last year, the market was down 13%. Within the top line figures, the market in September was around 40% lower than July and August, but initial indications are that the market is picking up again in October.

Despite ongoing challenges, the UK subcontract manufacturing market held steady in Q3 of 2022 / Picture: Getty/iStock

The CMI is produced by sourcing specialist Qimtek and reflects the total purchasing budget for outsourced manufacturing of companies looking to place business in any given month. This represents a sample of over 4,000 companies that could be placing business that together have a purchasing budget of more than £3.4bn and a supplier base of over 7,000 companies with a verified turnover in excess of £25bn.

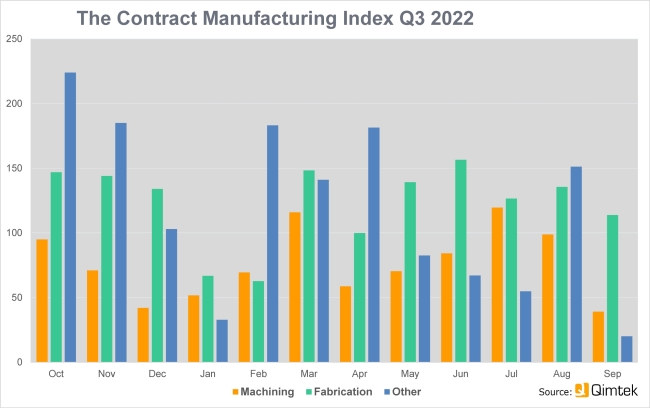

The baseline for the index is 100, which represents the average size of the subcontract manufacturing market between 2014 and 2018. Comparing types of subcontracting, there were sharp differences between machining and fabrication. The machining market dropped sharply throughout the quarter, falling by two thirds from July to September, but was still up 20% on the previous quarter.

In contrast, fabrication held relatively steady across the quarter, but was down 6% on the previous three months. Machining accounted for 39% of the total market with fabrication accounting for 54%. Other processes, such as moulding and assembly, accounted for the remainder.

As in Q1 and Q2, the strongest sector was industrial machinery which grew a further 67% on top of the 10% increase from Q1 to Q2. The second strongest sector was again food and beverage, with construction growing by 50% to move into the third position. Strong growth in oil/chemical/energy saw it move from thirteenth to fifth.

Qimtek owner Karl Wigart, said: “Although the overall figures suggest that the market has steadied, there is still a lot of turbulence and uncertainty out there. The quarter started well but September was very slow across all categories due to a lack of activity in the market. Buyers were obviously waiting to see what the new government would bring and the market was also disrupted by the sad news of the Queen’s death. October is much better but we have many buyers who are still waiting for clarification and are postponing new projects.”

Graphic & data courtesy of Qimtek